APPLETON, Wis. — As the end of the year approaches, millions of Americans are scrambling to spend down their Flexible Spending Account balances before the funds expire under the longstanding 'use it or lose it' rule. This financial tool, designed to help workers set aside pre-tax dollars for medical and dependent care expenses, often leaves participants with unused money that vanishes if not utilized by the deadline, typically December 31.

According to CBS News financial contributor Carmen Wong Ulrich, who recently addressed the topic in a segment titled 'Flex Spending: How to use it and not lose it,' getting the most out of a Flexible Spending Account requires careful planning and awareness of eligible expenses. 'How can you get the most out of a Flex Spending Account?' Ulrich posed in the report, emphasizing the importance of strategic use to avoid forfeiting hard-earned savings.

Flexible Spending Accounts, or FSAs, have been a staple of employee benefits packages since their inception in the 1970s under Section 125 of the Internal Revenue Code. Employers offer them as part of cafeteria plans, allowing workers to contribute up to $3,200 in 2024 for health care FSAs or $5,000 for dependent care versions, all deducted pre-tax to reduce taxable income. The catch, however, is the annual forfeiture rule: any unspent funds revert to the employer at year's end, a policy that critics argue discourages participation despite the tax advantages.

Ulrich, speaking directly to viewers in the CBS News video, highlighted common pitfalls. She explained that many people overestimate their medical needs when enrolling at the start of the year, leading to surplus funds. 'CBS News financial contributor Carmen Wong Ulrich speaks to the,' the segment begins, delving into practical advice for maximization. One key tip she offered is to review recent receipts for eligible out-of-pocket costs like copays, deductibles, and over-the-counter medications such as bandages or sunscreen, which qualify under IRS guidelines.

In Appleton, local human resources experts echo this sentiment. Sarah Jenkins, benefits coordinator at Fox River Manufacturing, a mid-sized employer in the area, said her office sees a spike in FSA-related inquiries every November. 'We've had employees come in asking about eyeglasses or orthodontia bills from earlier in the year,' Jenkins noted. 'It's frustrating when they realize they could have used their FSA for that laser eye surgery last spring.'

The IRS provides a detailed list of qualified expenses, updated annually. For 2024, this includes everything from acupuncture sessions to fertility treatments, as well as childcare costs for dependents under 13 in dependent care FSAs. Ulrich stressed in her commentary the value of submitting claims promptly, as reimbursements can take weeks to process. She advised setting aside a calendar reminder for mid-December to tally potential expenses, ensuring no dollars go to waste.

Recent changes to FSA rules offer some relief from the strict forfeiture policy. Since 2013, a carryover provision allows up to $640 of unused health FSA funds to roll over to the next year, provided the plan permits it. Additionally, a grace period of up to 2.5 months into the new year can extend the spending window. However, not all employers adopt these options; a 2023 survey by the Employers Council on Flexible Compensation found that only 40% of plans include carryover, leaving many participants vulnerable to losses.

'The key is education,' Ulrich said in the CBS segment. 'People need to know what counts — things like contact lenses, hearing aids, even certain transportation costs to medical appointments. Don't let your money expire without purpose.'

Local stories illustrate the real-world impact. Take Mark Thompson, a 42-year-old teacher at Appleton North High School, who contributed $2,500 to his health FSA this year. In late November, he visited his optometrist for new progressive lenses, reimbursing $450 through his account just in time. 'I almost forgot about the dental cleaning from October,' Thompson shared. 'My HR rep reminded me, and it saved me from losing a couple hundred bucks.'

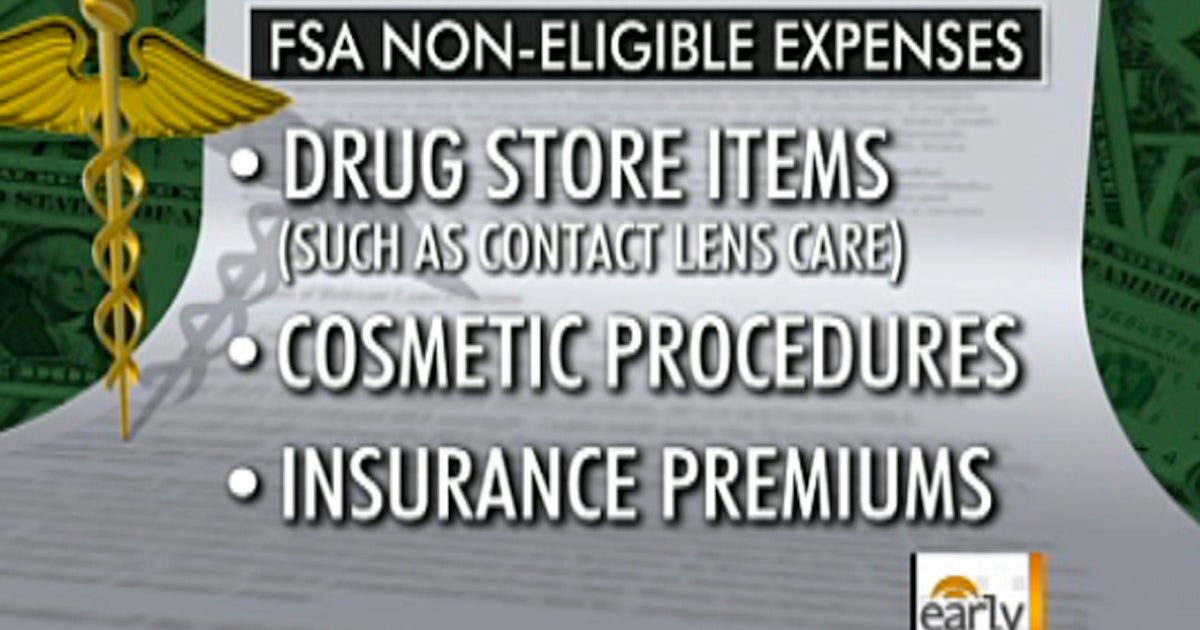

Experts like Ulrich also warn against common misconceptions. For instance, cosmetic procedures such as Botox are generally ineligible unless medically necessary, like for migraines. Gym memberships might qualify if prescribed for a specific condition, but broad wellness expenses do not. The IRS Publication 502, updated for 2024, serves as the definitive guide, and Ulrich recommended consulting it alongside plan documents.

Beyond individual losses, the broader economic implications are significant. The Employee Benefit Research Institute estimates that Americans forfeit about $2 billion in FSA funds annually, money that could alleviate healthcare costs amid rising premiums. In Wisconsin, where average family health insurance deductibles exceed $3,000, FSAs represent a crucial buffer. State officials, including those at the Department of Workforce Development, promote FSA awareness through employer workshops, but uptake remains uneven, particularly among small businesses.

Ulrich's segment, aired on CBS News in early December 2023, timed its release to coincide with open enrollment season, when workers select benefits for the coming year. She interviewed plan administrators who reported that underutilization stems from lack of communication. 'Employers should be proactive,' one anonymous HR professional told her. 'Send monthly reminders about balances — it makes a difference.'

As Appleton residents navigate this fiscal hurdle, community resources are stepping up. The Fox Cities United Way hosts free financial literacy sessions, including FSA breakdowns, at the Appleton Public Library on December 15 and 20. Coordinator Lisa Ramirez said attendance has doubled this year. 'We're seeing more questions about dependent care FSAs, especially with childcare shortages,' she observed.

Looking ahead, potential legislative tweaks could reshape FSAs. Bipartisan bills in Congress aim to increase contribution limits and expand eligible expenses to include menstrual products and telehealth fees, building on pandemic-era flexibilities. For now, though, the onus falls on individuals. Ulrich wrapped her advice with a call to action: Review your balance today, she urged, and turn potential losses into tangible benefits.

In the end, mastering the FSA isn't just about saving taxes — it's about reclaiming control over healthcare dollars in an unpredictable economy. As one Appleton accountant put it, 'It's free money if you use it right.' With deadlines looming, the message is clear: Act now, or watch it slip away.