As Americans across the country receive their tax refunds this spring, financial experts are emphasizing the importance of using these windfalls wisely amid ongoing economic uncertainties. According to a recent segment on NBC's TODAY show, the average tax refund for the 2026 tax year stands at nearly $3,400, providing a timely opportunity for individuals to strengthen their financial footing. NBC business correspondent Christine Romans joined the program on April 21, 2026, to offer practical advice on how to allocate these funds effectively, focusing on strategies that prioritize long-term stability over short-term indulgences.

Romans, a veteran journalist known for her coverage of personal finance and economic trends, highlighted the segment's relevance in a time when inflation remains a concern for many households. 'The average tax refund this year is nearly $3,400,' she stated during the broadcast, underscoring the potential impact of even modest sums when directed thoughtfully. Her appearance came as the Internal Revenue Service reported that refunds began processing earlier than in previous years, with millions already deposited into bank accounts by mid-April.

The discussion on TODAY, hosted by popular anchors, delved into the broader context of tax season 2026, which saw adjustments to filing deadlines due to lingering effects from the previous year's natural disasters in several states. While the IRS has not released comprehensive data on total refunds yet, early indicators suggest a slight increase from 2025's average of around $3,200, attributed to updated withholding tables and expanded child tax credits. Romans' tips, drawn from consultations with financial planners and economic analysts, aim to address common pitfalls like impulse spending that often erode these gains.

One of the primary recommendations from Romans is to build or bolster an emergency fund. In an era where unexpected expenses—from medical bills to car repairs—can derail budgets, she advised setting aside at least three to six months' worth of living expenses. 'Building an emergency fund is crucial,' Romans explained, noting that surveys from financial institutions like Bankrate indicate nearly 60 percent of Americans couldn't cover a $1,000 emergency without borrowing. For those receiving the average $3,400 refund, she suggested directing 20 to 30 percent—roughly $680 to $1,020—toward a high-yield savings account, where current rates hover around 4 to 5 percent annually.

This advice resonates with reports from the Federal Reserve, which in its latest consumer credit survey painted a picture of strained household finances, with credit card debt reaching record highs of over $1 trillion nationwide. Romans emphasized that an emergency fund acts as a buffer against such vulnerabilities, potentially preventing reliance on high-interest loans. Viewers tuning into the TODAY segment, which aired at 8:15 a.m. Eastern Time, shared immediate feedback on social media, with many praising the simplicity of the approach for families in mid-sized cities like Appleton, Wisconsin, where living costs are rising but wages lag behind coastal areas.

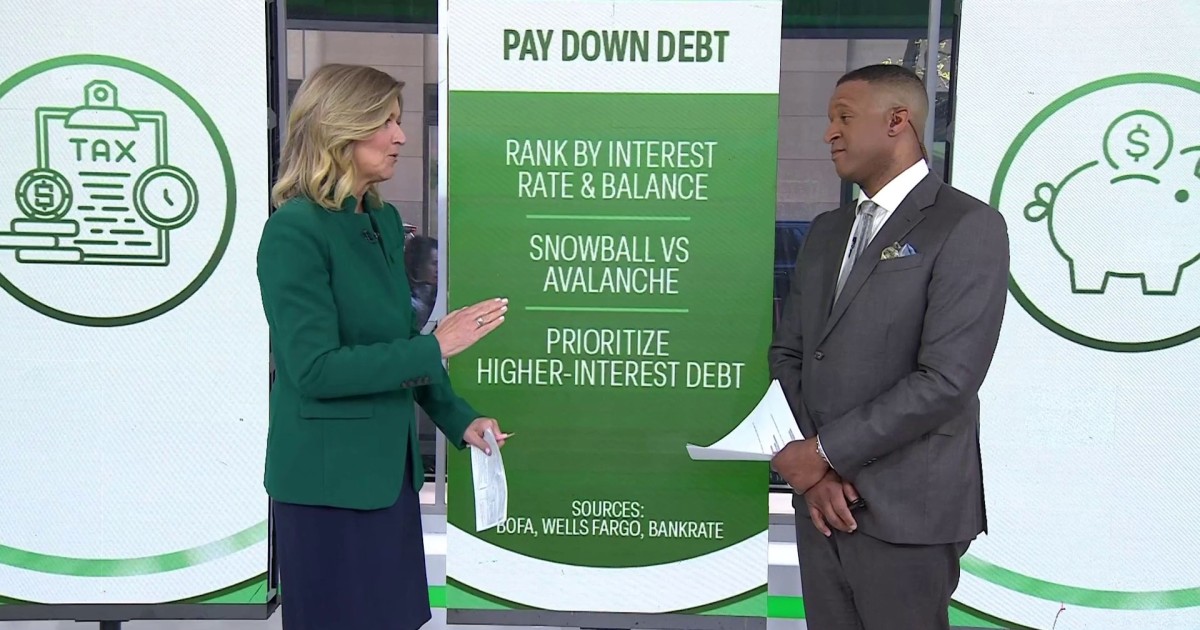

Paying down debt emerged as Romans' second key tip, particularly targeting high-interest obligations like credit cards and personal loans. With average credit card interest rates exceeding 20 percent, she warned that carrying balances can quickly diminish the value of a tax refund. 'Paying down debt should be a priority,' Romans said, recommending the 'debt snowball' method—focusing on smallest balances first for psychological wins—over more complex strategies unless advised by a professional. According to data from the Consumer Financial Protection Bureau, Americans collectively owe more than $4.5 trillion in non-mortgage debt, making this step vital for regaining control.

In the segment, Romans shared an anecdote from a focus group of young professionals in New York, where participants described how using past refunds to chip away at student loans averaging $30,000 per borrower led to measurable relief. She cautioned, however, that not all debt is equal; low-interest mortgages or federal student loans might warrant less urgency compared to revolving credit. This nuanced view aligns with guidance from nonprofit credit counseling agencies, which report a 15 percent uptick in consultations during tax season as people reassess their finances.

Beyond immediate necessities, Romans advocated for boosting overall savings, including contributions to retirement accounts. With the 2026 contribution limits for 401(k)s raised to $23,500 for those under 50, she encouraged viewers to consider direct transfers to IRAs or employer-sponsored plans to capitalize on tax advantages. 'Boosting savings is an investment in your future,' she noted, pointing to compound interest as a powerful tool—$3,400 invested at 7 percent annual return could grow to over $10,000 in 15 years. This recommendation comes at a time when retirement readiness remains a national concern, with the Social Security Administration projecting trust fund depletion by 2035 without personal savings supplements.

The TODAY broadcast also touched on additional uses for refunds, such as funding education or home improvements, though Romans stressed these should follow the foundational steps of emergency savings and debt reduction. For instance, she mentioned the benefits of Health Savings Accounts (HSAs) for those with high-deductible insurance plans, where contributions are tax-deductible and withdrawals for medical expenses tax-free. In 2026, HSA limits increased to $4,150 for individuals, offering another avenue for the average refund to yield long-term benefits.

Contextually, the segment aired amid discussions in Washington about potential tax code reforms, with bipartisan proposals floating ideas like automatic savings allocations for refunds. Economists from the Brookings Institution have supported such measures, arguing they could help close the racial wealth gap, where Black and Hispanic households hold median savings under $5,000 compared to over $40,000 for white families. Romans acknowledged these disparities, suggesting community-based financial literacy programs as a complementary resource.

Critics of aggressive debt payoff strategies, including some personal finance bloggers, argue that investing during market upswings might outpace interest savings, but Romans countered that psychological security from reduced debt often outweighs speculative gains. 'Everyone's situation is unique,' she said, urging consultation with certified financial planners through organizations like the Financial Planning Association. This balanced perspective reflects the segment's aim to empower rather than prescribe, resonating with TODAY's audience of primarily working parents and young adults.

As tax refunds continue to roll out— with the IRS expecting to process over 150 million returns by the April 15 deadline extension—Romans' advice serves as a roadmap for navigating post-pandemic recovery. Economic indicators from the Bureau of Labor Statistics show unemployment at 3.8 percent, yet wage growth at just 4.1 percent, squeezing disposable income. By directing refunds strategically, individuals can mitigate these pressures, potentially contributing to broader economic stability.

Looking ahead, financial experts anticipate that 2027 tax policies could influence refund sizes, with debates over eliminating certain deductions gaining traction in Congress. For now, Romans' TODAY appearance stands as a timely reminder of the refund's potential as a catalyst for positive change. As one viewer commented online, 'Finally, practical steps that don't feel overwhelming.' With summer spending temptations looming, the message is clear: thoughtful allocation today can secure brighter prospects tomorrow.

In Appleton and similar communities, local banks have reported a surge in savings account openings following similar media coverage, indicating the ripple effect of national advice on everyday lives. Romans concluded the segment by encouraging viewers to track their progress with free budgeting apps, reinforcing that small, consistent actions build lasting wealth.